Proactive vs. Reactive Risk Management: A Closer Look at Financial Institutions and Banks

Introduction

Operational risk is an inherent aspect of the financial industry, encompassing a wide range of potential hazards, from technological failures and cyber threats to human errors and regulatory non-compliance. The management of operational risk is crucial for financial institutions and banks, as it directly impacts their stability, reputation, and overall performance. In this article, we will explore whether financial institutions and banks are proactively managing operational risk or if they tend to adopt a reactive approach.

Understanding Proactive and Reactive Risk Management

Proactive Risk Management:

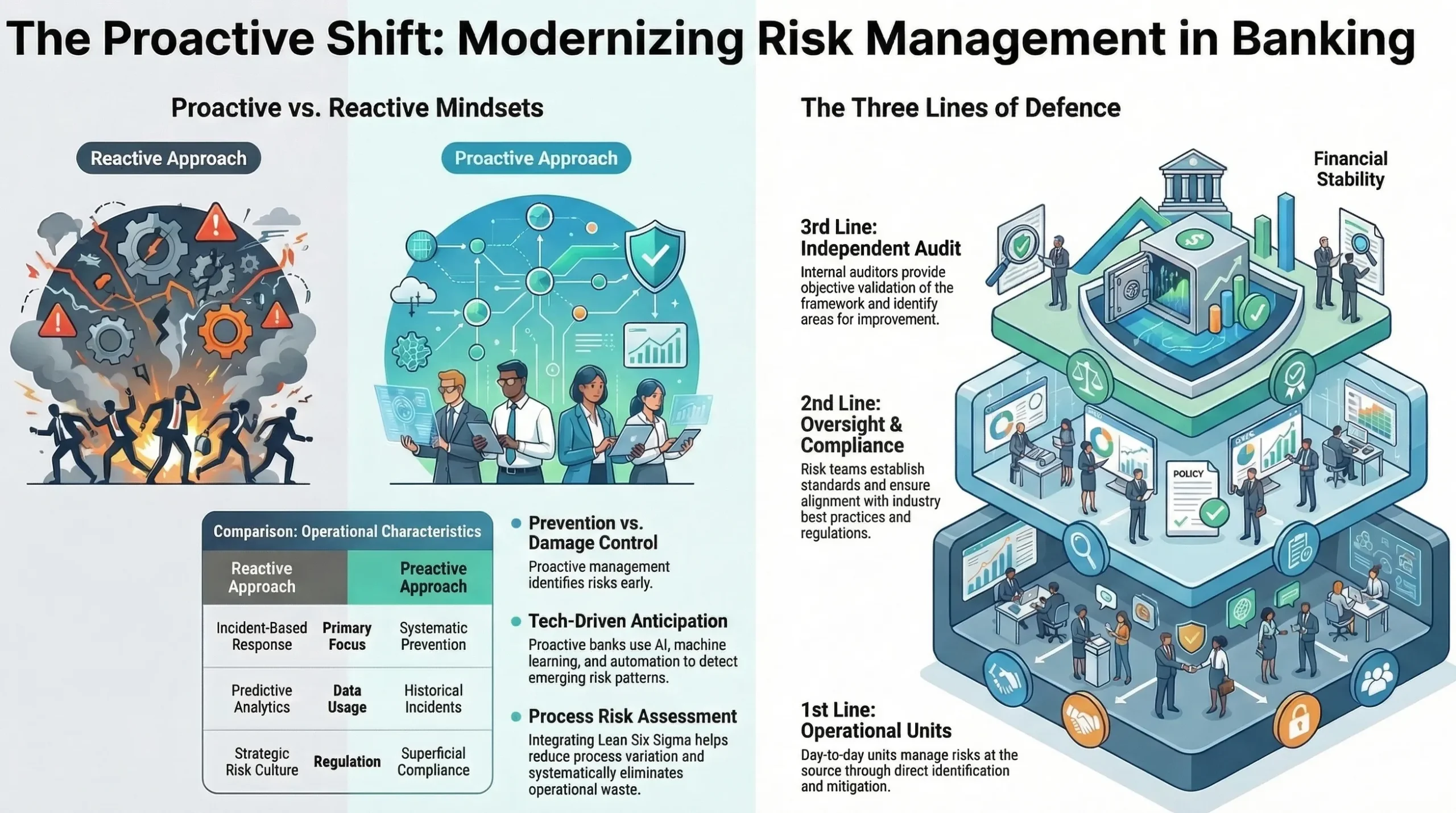

Proactive risk management involves the identification, assessment, and mitigation of potential risks before they materialize into significant issues. Financial institutions that embrace a proactive approach to risk management are forward-thinking, systematic, and emphasize prevention. They establish comprehensive risk frameworks, conduct regular risk assessments, and prioritize risk-mitigating strategies.

Reactive Risk Management:

On the other hand, reactive risk management refers to the handling of risks after they have already occurred, often in response to an adverse event or crisis. Reactive institutions are more likely to focus on damage control and remediation rather than pre-emptively addressing potential risks. This approach can lead to higher costs, reputational damage, and regulatory scrutiny.

Proactivity in Operational Risk Management

There are options to employ two parallel approaches to Operational Risk Management, either independently or in combination, depending on the specific requirements of the industry:

- Operational Risk Framework

- Process Risk Assessment

- Operational Risk Framework: This approach is widely embraced in the banking industry, built upon established industry best practices such as Failure Mode and Effects Analysis (FMEA). The elements outlined below, including risk culture governance, data analytics, control automation, and scenario planning, represent a comprehensive enhancement of risk assessment’s effectiveness through the integration of cutting-edge technological advancements.

- Risk Culture and Governance: Proactive institutions prioritize a strong risk culture and robust governance structures. They instil risk awareness and accountability across all levels of the organization, encouraging employees to report potential risks and suggest improvements. Regular risk reviews and audits ensure compliance with policies and standards.

- Data Analytics and Technology: Proactive risk management heavily relies on data analytics and advanced technology. Financial institutions invest in sophisticated risk models, to detect patterns and anticipate emerging risks. This data-driven approach enables faster decision-making and early detection of potential issues.

- Controls Automation: By using artificial intelligence, and machine learning algorithms, financial institutions and banks can automate manual preventative controls. This would pave way for reliable potential risk exposure being identified proactively. The white paper on “Controls Automation” provides valuable insights on how organizations can embrace technologies to identify and mitigate risks proactively. Click on the link for details: https://www.linkedin.com/posts/rameshgopalan_controls-testing-automation-white-paper-activity-6745185922884734976-6hj7?utm_source=share&utm_medium=member_desktop

- Scenario Planning: Forward-thinking institutions conduct scenario planning exercises to assess the impact of potential risks on their operations. These simulations help them devise effective risk response strategies and enhance their resilience in the face of adverse events.

- Process Risk Assessment: Lean Six Sigma, a powerful methodology for process improvement, can be a valuable tool in enhancing process risk assessment efforts. By integrating Lean principles, which focuses on waste reduction and efficiency, with Six Sigma’s emphasis on reducing variation and defects, organizations can systematically identify, analyse, and mitigate risks within processes. This approach not only helps in proactively addressing potential issues but also enhances overall process performance, quality, and customer satisfaction. By harnessing the synergy between Lean Six Sigma and risk assessment, organizations can drive better decision-making, optimize resource allocation, and strengthen their competitive advantage in a dynamic business landscape.

Reactivity in Operational Risk Management

- Incident-Based Approach: Reactive institutions often rely on historical incidents to drive risk management decisions. This approach may overlook emerging risks and fail to address systemic issues that could lead to recurring problems.

- Regulatory Compliance Focus: Some institutions may only prioritize risk management to meet regulatory requirements. While compliance is essential, solely focusing on satisfying regulatory demands can lead to a superficial approach to risk management. Regulatory risks should be treated like any other risk.

- Decision Making: Reactive institutions may respond hastily during a crisis, making decisions in a pressured environment that could have long-term consequences. Proactive planning, however, allows for a more measured and thoughtful response.

Let us explore the significance of the Three Lines of Defence teams in a bank and how they can contribute to implementing proactive operational risk management.

1. Understanding the Three Lines of Defence Model:

The Three Lines of Defence model is a risk management framework that establishes clear accountabilities and responsibilities across the bank’s operational risk management process. It delineates three distinct lines of defence:

First Line of Defence: The first line of defence includes the operational units responsible for executing day-to-day activities. These units directly manage operational risks as part of their daily operations. They have a direct impact on risk exposures and are best positioned to identify, assess, and mitigate operational risks at their source.

Second Line of Defence: The second line of defence comprises risk management and compliance functions. These teams provide oversight and support to the first line of defence. They establish risk management policies, procedures, and standards, monitor the bank’s risk exposure, and ensure compliance with internal and external regulations.

Third Line of Defence: The third line of defence consists of the internal audit function. Internal auditors are independent from the first and second lines and provide objective evaluations of the bank’s risk management processes and controls. They assess whether the risk management framework is effective and identify areas for improvement.

2. Advantages of the Three Lines of Defence Model in Proactive Risk Management:

Proactive operational risk management is about identifying and addressing potential risks before they escalate into issues that can harm the bank’s reputation, financial stability, or customer trust. The Three Lines of Defence model can play a pivotal role in fostering a proactive risk management culture:

a. Risk Awareness:

The first line of defence teams are at the forefront of operational activities and are in the best position to identify potential risks as they emerge. By empowering these teams to be accountable for managing risks, the bank creates a culture of risk awareness at all levels. This increased vigilance helps in the early detection of risks, enabling timely actions to prevent or mitigate potential adverse events.

b. Risk Oversight:

The second line of defence teams, consisting of risk management and compliance experts, provide essential oversight and support to the first line. They ensure that the bank’s operational risk management processes are aligned with industry best practices, regulatory requirements, and internal policies. This oversight ensures that risk management practices are comprehensive, consistent, and responsive to emerging risks.

c. Independent Validation:

The third line of defence, represented by internal auditors, provides an impartial and objective assessment of the bank’s risk management activities. They validate the effectiveness of the risk management framework and provide assurance to senior management and the board that operational risks are being adequately addressed. Their independent evaluations identify gaps and areas for improvement, facilitating continuous enhancement of risk management practices.

d. Proactive Risk Mitigation:

By incorporating the Three Lines of Defence model, banks can detect and address potential operational risks early in the risk lifecycle. This proactive approach will enable banks to take preventive measures and implement controls (automated, wherever possible) to minimize the likelihood and impact of risks. As a result, the bank becomes more resilient and better positioned to navigate uncertainties in the ever-evolving financial landscape.

e. Continuous Improvement:

The Three Lines of Defence model should promote a culture of continuous improvement in operational risk management. Through regular feedback, communication, and collaboration among the three lines, banks can learn from incidents, refine risk management strategies, and enhance overall risk preparedness over time.

Conclusion

The successful management of operational risk is vital for the stability and sustainability of financial institutions and banks. In the highly dynamic and risk-prone banking industry, proactive operational risk management is a strategic imperative. While some institutions have embraced a proactive approach to risk management by investing in advanced technology, fostering a strong risk culture, and conducting scenario planning, others still operate with a more reactive mindset, responding to incidents after they occur.

To achieve a truly resilient risk management framework, financial institutions and banks must aim to be proactive in their approach. By continuously assessing and mitigating potential risks, they can build a solid foundation that enables them to navigate challenges effectively and seize new opportunities with confidence. We welcome your valuable inputs, comments, and thoughts on how organizations can move from reactive to proactive risk management.

Ramesh Gopalan

www.linkedin.com/in/rameshgopalan